- Rare Earths

- Semiconductors

- U.S.-China

Trump Brings Wall Street and Silicon Valley to Beijing Summit

12 minute read

President Trump’s Beijing summit brings Apple, NVIDIA, Tesla, and BlackRock to the table, signaling that American corporate power is now inseparable from diplomatic strategy.

Key Takeaways

- Trump arrived in Beijing with a delegation spanning Apple, NVIDIA, Tesla, BlackRock, and Boeing, reflecting how deeply American corporate interests are now woven into high-level diplomatic engagement with China.

- Talks are expected to focus on extending the late-2025 rare earth trade truce, clarifying semiconductor export pathways, and establishing more predictable bilateral trade and investment channels.

- Markets responded positively to the delegation’s composition, with NVIDIA, Tesla, and Apple equities showing resilience as investors priced in incremental progress rather than transformative agreement.

When the Boardroom Meets the Diplomatic Table

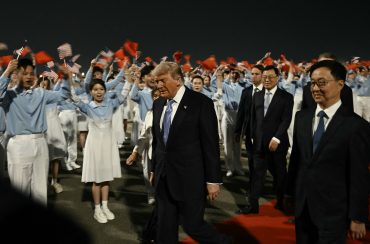

BEIJING, China — President Donald Trump landed in Beijing on Wednesday for his first state visit to China in nearly a decade, and the delegation he brought tells the story more plainly than any prepared statement. Tim Cook, Jensen Huang, Elon Musk, Larry Fink, and the senior leadership of Boeing, Goldman Sachs, Citigroup, Qualcomm, Micron, Visa, Mastercard, and Cargill made the journey. In scope and symbolic weight, the group is without precedent in recent American diplomatic history. These are not trade representatives or policy advisers. They are the architects of the economic architecture that binds the two largest economies on earth, and their presence in Beijing reflects a reality that neither capital can afford to ignore: the bilateral relationship is now too structurally embedded to be managed by governments alone.

The visit, delayed earlier this year by the conflict in Iran, arrives at a moment of deliberate equilibrium. Tariffs remain elevated, export controls on advanced semiconductors continue to constrain commerce, and the long-range tensions over Taiwan and regional stability have not dissolved. Yet the dominant register of this summit, established by both delegations before a single formal session has convened, is transactional. The message from Washington and Beijing alike is that the costs of escalation now exceed whatever strategic advantage either side imagined it could extract.

The Numbers Behind the Presence

The delegation is not ceremonial. Each executive carries specific financial exposure that gives the summit its commercial gravity and its sense of urgency.

Apple’s Tim Cook arrives having just reported $20.5 billion in Greater China revenue for the fiscal second quarter ended March 28, 2026, a 28% year-on-year increase driven by sustained iPhone demand. No restructuring exercise, however ambitious, removes China from Apple’s near-term architecture. The country remains the assembly base for a significant share of global device production and one of the company’s most consequential revenue markets. For Cook, any regulatory clarity that emerges from this summit translates directly into supply security and earnings stability. His presence is less diplomatic gesture than operational necessity.

Jensen Huang’s inclusion was confirmed late, and the market responded with precision. NVIDIA shares rose in overnight trading after his travel was announced, as investors interpreted his seat at the table as evidence that semiconductor access is a live agenda item rather than a frozen dispute. NVIDIA’s China revenue accounted for roughly 13% of total sales in fiscal 2025 before successive export control rounds sharply compressed that figure. The limited approval of H200 chip exports under strict licensing conditions opened a narrow channel. Huang’s presence in Beijing suggests that channel is under active negotiation.

Elon Musk travels on the strength of genuine momentum. Tesla’s Shanghai Gigafactory shipped 79,478 vehicles in April 2026, a 36% year-on-year increase, making China central not just to the company’s manufacturing footprint but to its global sales recovery. Larry Fink of BlackRock brings a different order of concern: capital flows, Chinese asset exposure, and the anxieties of an institutional investment community that has watched bilateral friction translate into portfolio volatility with increasing regularity. Boeing attends with multibillion-dollar aircraft orders within range, in a market where competition from domestic Chinese manufacturers is tightening by the year.

Taken together, the delegation maps the precise anatomy of U.S.-China interdependence. These are not companies exploring a new relationship. They are businesses whose current valuations, supply structures, and long-range growth assumptions are already built on bilateral ties that took decades to construct and cannot be dismantled without consequences that neither side has shown any serious willingness to absorb.

The Core Issues

The most time-sensitive is the extension of the late-2025 rare earth trade truce. China controls the dominant share of global rare earth mineral processing, and those materials are essential inputs for electric vehicles, advanced defense systems, and renewable energy infrastructure. The existing arrangement exchanged Chinese mineral and magnet flows for moderated U.S. tariffs. American officials have indicated confidence that an extension will be reached, though formal announcement timing remains fluid. For manufacturers across the defense and clean energy supply chain, continuity is not an abstraction. It is a production schedule.

Semiconductor policy is the more complex terrain. Export controls have suppressed NVIDIA’s China access and introduced persistent uncertainty across the broader technology supply chain. The realistic path forward is not resolution but structured management: clearer licensing frameworks, formal bilateral communication channels that reduce the risk of abrupt regulatory shifts, and possibly the establishment of dedicated trade and investment boards designed to handle friction with greater predictability. Both governments are simultaneously pursuing strategic self-sufficiency — the U.S. through domestic chip incentives and allied sourcing partnerships, China through accelerated indigenous semiconductor development — and neither is close to achieving it. The best available outcome at this summit is a more navigable competition, not its end.

Artificial intelligence forms the third strand, deliberately ambiguous in its framing. The presence of Huang alongside senior officials from both sides signals that AI has crossed into the domain of bilateral economic policy, even as national security restrictions continue to govern what can be transferred and under what conditions. No formal framework is expected to emerge, but the conversation itself represents a shift from avoidance to engagement on a topic that will define the relationship’s technological dimension for years.

Reading the Market Signals

Financial markets delivered a preliminary judgment before the summit formally opened. NVIDIA’s overnight gains following Huang’s confirmed attendance reflect a specific institutional bet: that his presence meaningfully increases the probability of progress on export licensing. Apple and Tesla equities showed resilience through the pre-summit session, consistent with investor appetite for de-escalation. Boeing’s inclusion in the delegation has been read by aerospace analysts as a precondition for substantive commercial negotiations with Chinese carriers, and the company’s leadership did not travel to Beijing to return empty-handed.

The reactions are measured rather than euphoric, which is the appropriate register. Institutional investors have observed enough high-profile bilateral encounters produce limited deliverables to approach each summit with discipline. The operative question is not whether this visit resolves the structural tensions in U.S.-China relations. It will not. The question is whether it produces durable, actionable agreements that reduce friction in specific domains — and even that narrower ambition must contend with the domestic political pressures in both capitals, where the language of strategic competition has become too entrenched to set aside.

A Mature Entanglement

What distinguishes this summit from earlier chapters in the bilateral relationship is the absence of pretense about fundamental convergence. Neither Washington nor Beijing is under the illusion that two days of meetings will harmonize competing strategic interests. What both appear to accept is that the relationship has grown too consequential, and too costly to rupture, to be governed by confrontation alone.

The business delegation is the clearest expression of that acceptance. These are companies whose revenue lines, supply chains, and capital allocation decisions already reflect the integration of two economies that have spent years attempting to define the terms of their competition. That effort has not produced clarity, but it has produced interdependence so deep that it now shapes the composition of presidential delegations. The boardroom and the summit table have, in the most literal sense, become the same room.

Whether the week ends with a formalized rare earth extension, incremental movement on semiconductor licensing, or the architecture of new investment dialogue, its significance is partly established before any agreement is signed. In 2026, American diplomacy with China cannot be cleanly separated from the interests of those who built and continue to operate the commercial ties that both nations depend on. That is not a vulnerability. It is the condition under which durable progress, when it comes, will have to be made.