- Deep Tech

- PsiQuantum

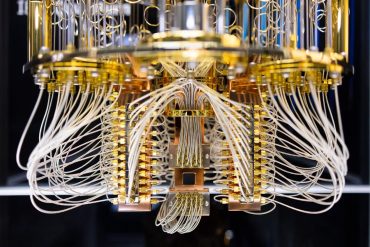

- Quantum Computing

Washington Backs Quantum at Scale With

$2 Billion Push

8 minute read

The U.S. government is deploying $2.013 billion across nine quantum companies, taking equity stakes and tying disbursements to hard milestones in a decisive industrial policy shift.

Key Takeaways

- The Commerce Department’s $2.013 billion commitment spans foundry infrastructure and competing quantum architectures, with IBM and GlobalFoundries anchoring the manufacturing build-out.

- Federal equity participation replaces passive grant-making with aligned incentives, giving Washington a direct financial stake in whether quantum computing reaches commercial scale this decade.

- Market reaction was immediate and substantial, with IBM rising 12 percent and pure-play names surging 20 to 30 percent, reflecting investor confidence in sovereign capital as a commercial de-risking mechanism.

A Portfolio, Not a Bet

The U.S. Department of Commerce issued letters of intent to distribute $2.013 billion in CHIPS and Science Act incentives to nine quantum computing companies, taking minority, non-controlling equity stakes in each. Commerce Secretary Howard Lutnick framed the announcement as opening a new era of American innovation. The more precise description is a structured industrial policy intervention, designed with the discipline of a portfolio rather than the optimism of a moonshot.

The architecture of the package reflects deliberate thinking about where the quantum supply chain actually breaks down. Two large awards address foundry infrastructure, the most persistent gap between laboratory demonstration and manufacturable hardware. IBM receives $1 billion to establish Anderon, a dedicated quantum wafer foundry in Albany, New York, focused on superconducting qubits and supporting electronics. IBM is matching the federal contribution dollar for dollar, supplementing it with intellectual property, assets, and personnel, and intends the facility to supply quantum wafers not only for its own systems but for the broader commercial ecosystem. GlobalFoundries, a trusted semiconductor manufacturer with established federal relationships, will receive $375 million to build a secure foundry capable of supporting multiple quantum modalities, including superconducting, trapped-ion, photonic, topological, and silicon spin architectures.

The remaining seven awards, each roughly $100 million, flow to specialist developers: Atom Computing and Infleqtion in neutral-atom systems, D-Wave across annealing and gate-model superconducting platforms, PsiQuantum in photonics, Quantinuum in trapped-ion, and Rigetti in superconducting. Diraq, the smallest recipient, receives up to $38 million. Each pursues a distinct technical path. That breadth is intentional.

The Equity Mechanism

The equity stakes are the structural feature that separates this program from previous federal quantum spending. The National Quantum Initiative Act, signed during President Trump’s first term, funded research. This round funds manufacturing and translation, and it does so with instruments that create accountability absent from grants. Washington now holds financial positions in companies whose technical milestones it helped define. Disbursements are tied to performance; clawbacks are possible if targets slip. The government has, in effect, moved from patron to co-investor.

That shift changes the incentive structure for all parties. Recipients face harder scrutiny than they would under research appropriations, and must demonstrate measurable progress toward fault-tolerant systems capable of addressing problems that classical supercomputers cannot. The target applications are not theoretical: molecular simulation for pharmaceuticals, materials design for energy and aerospace, optimization for logistics and finance, and cryptographic security for national defense. These are commercial and strategic priorities, not academic exercises. The equity mechanism aligns the interests of federal administrators and private executives around the same outcome: real, deployable quantum hardware.

Where the Field Stands

Quantum computing remains in the noisy intermediate-scale era. Error rates and system sizes have not yet crossed the threshold for consistent, large-scale computational advantage over classical machines. The distance between today’s best prototypes and commercially viable fault-tolerant systems is real and has, until recently, been measured in decades rather than years. IBM has publicly targeted demonstrations of quantum advantage in targeted applications by the end of 2026 and commercial fault-tolerant systems by 2029. The federal commitment is structured to underwrite that timeline.

China has invested heavily in its own programs. Europe and other allied economies have advanced targeted initiatives. The United States has held a durable lead in foundational research and private-sector innovation, but the transition to manufacturable, deployable hardware has exposed fragilities in supply chains and talent pipelines. By funding both competing modalities and the foundries that will build them, the administration is attempting to compress what would otherwise be extended, capital-intensive development cycles.

Market Response and Strategic Signal

Financial markets processed the announcement quickly. IBM shares rose as much as 12 percent on May 21. GlobalFoundries climbed roughly 15 percent. Among the pure-play names, gains were steeper: Infleqtion, Rigetti, and D-Wave each surged 20 to 30 percent or more during intraday trading. The moves recalled earlier CHIPS Act announcements that lifted semiconductor valuations broadly. Investors appear to read government validation and committed capital as powerful risk-reduction signals in a sector where technical breakthroughs have historically been followed by extended, expensive commercialization periods. Rigetti’s recent Cepheus-1 multi-chip demonstration and D-Wave’s dual-platform progress added operational context to the enthusiasm.

The underlying economics justify the attention. Quantum computing’s commercial potential, by various estimates, could reach hundreds of billions of dollars by 2040 across pharmaceuticals, materials, logistics, and financial modeling. Sovereign capital reduces the probability of the Valley of Death scenario that has extinguished earlier deep-technology waves.

Manufacturing Phase

Letters of intent are not final awards. Due diligence, milestone negotiations, and formal agreements lie ahead. The government’s equity positions, while structured to avoid operational control, introduce new oversight dynamics that will require careful management on both sides. Success will ultimately hinge on execution speed, talent retention, and the ability of these companies to convert federal capital into proprietary breakthroughs rather than incremental improvements on existing architectures.

The program’s bipartisan foundations are worth noting. The underlying CHIPS and Science Act was signed in 2022 under the previous administration and enjoyed broad congressional support precisely because quantum leadership is viewed as a non-partisan national security and economic imperative. The Trump White House has made the initiative its own, folding it into a wider pattern of assertive industrial policy that includes direct equity participation in strategically critical sectors. The philosophy is consistent: reduce foreign dependency, secure supply chains, and compress the timeline from invention to deployment.

What is not ambiguous is the directional commitment. By pairing foundry investment with a diversified technology portfolio, Washington has signaled that it intends to lead not just in quantum research but in quantum production. The institutions, capital structures, and manufacturing infrastructure being assembled now will shape which nation sets the commercial and security terms of the quantum era. The United States has put substantial capital behind the proposition that this decade will settle it.