- Agentic AI

- Cloud Platforms

- Data Infrastructure

- Enterprise AI

Snowflake Breaks Out as the Agentic Enterprise Takes Shape

9 minute read

Snowflake’s strongest sequential growth quarter on record, a $6 billion AWS commitment, and the acquisition of Natoma signal a decisive pivot toward governing enterprise AI at scale.

Key Takeaways

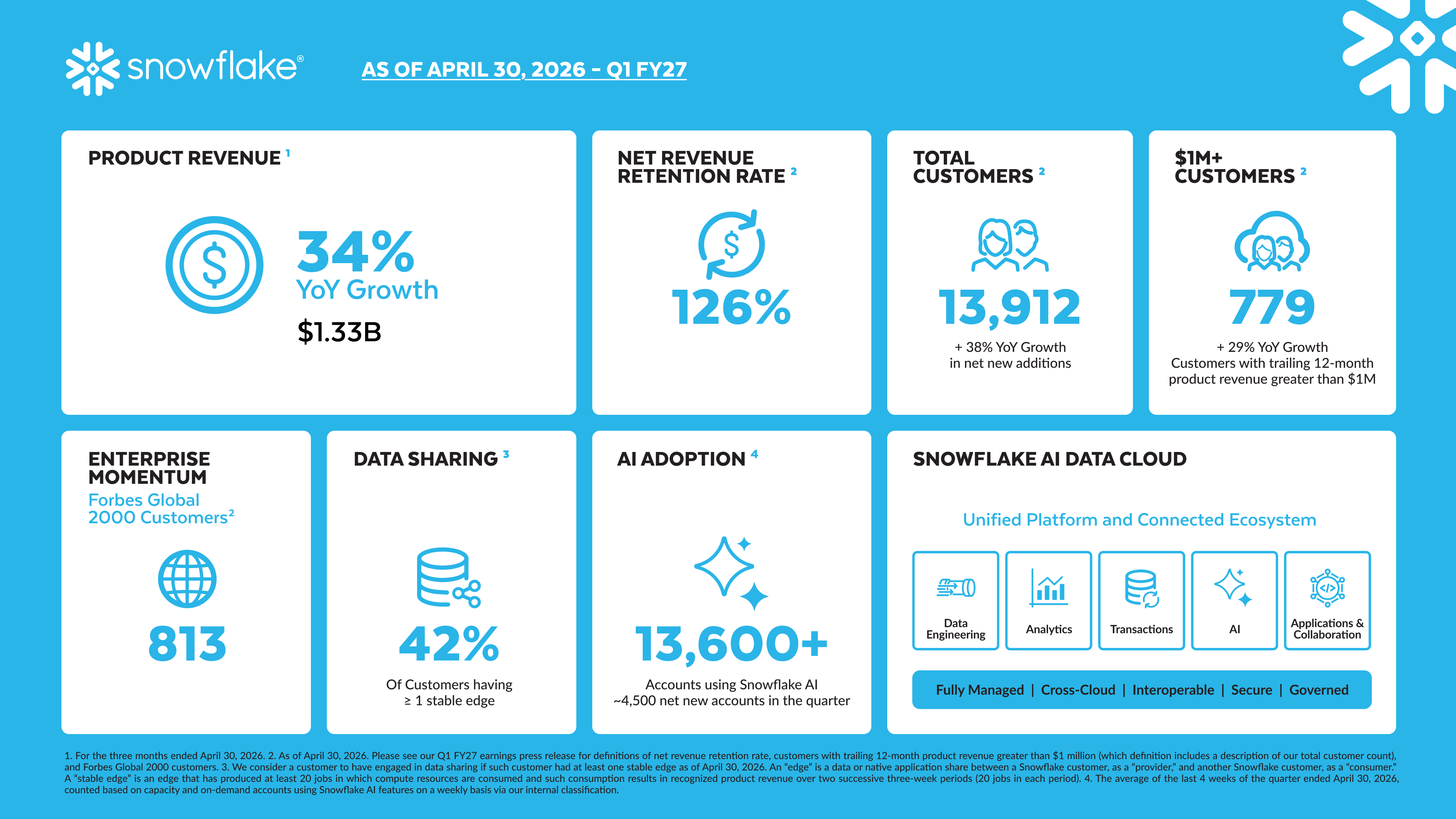

- Product revenue grew 34% year-over-year to $1.334 billion, the company’s strongest sequential dollar growth on record, with full-year guidance raised to $5.84 billion and non-GAAP operating margin targets lifted to 13.5%.

- A $6 billion multi-year AWS infrastructure commitment and the pending acquisition of Natoma, an enterprise Model Context Protocol platform, position Snowflake to govern both the data and action layers of enterprise AI deployments.

- With net revenue retention at 126%, remaining performance obligations up 38% to $9.21 billion, and AI product adoption accelerating sharply, Snowflake’s growth reacceleration appears structural rather than episodic.

A Quarter That Clarifies the Thesis

For a company that spent much of the past two years navigating investor skepticism about growth durability and strategic coherence, Snowflake’s first quarter of fiscal year 2027 delivered something more consequential than a beat-and-raise. It delivered a thesis.

Product revenue of $1.334 billion rose 34% year-over-year, marking a clear acceleration from the mid-to-high-20s growth rates that characterized recent periods. Total revenue reached $1.391 billion, up 33%. Non-GAAP diluted earnings per share of $0.39 exceeded consensus, and non-GAAP operating margin expanded to 11.9%. These are not incremental improvements. Against the backdrop of an enterprise technology market where procurement caution has been a persistent drag, they constitute a material shift in the company’s trajectory.

Snowflake Inc. (NASDAQ: SNOW) shares closed at $175.26 on May 27. After-hours trading saw gains of 25 to 37 percent as investors absorbed not just the financial results but the strategic moves announced alongside them.

The Infrastructure Commitment as Signal

On the same day as its earnings release, Snowflake announced a $6 billion multi-year commitment to AWS, its largest infrastructure agreement to date, targeting Graviton processors and AI accelerators specifically designed to support agentic workloads. The scale of the commitment warrants attention.

Infrastructure agreements of this magnitude are simultaneously a declaration of demand conviction and a mechanism for locking in capacity and pricing discipline. For Snowflake, which operates across a multi-cloud environment, deepening its AWS alignment carries both strategic and commercial logic. A growing share of enterprise software procurement now flows through hyperscaler marketplaces, and AWS Marketplace already routes meaningful revenue to Snowflake. The $6 billion figure signals that management expects compute-intensive AI workloads to grow substantially and wants the infrastructure in place to support them without constraint.

It also reflects a broader competitive reality. In the race to serve enterprise AI at production scale, infrastructure predictability is itself a differentiator. Customers building agentic systems that must act reliably across internal tools and external APIs cannot absorb supply-side friction. By securing capacity ahead of demand, Snowflake is positioning itself to make performance commitments that smaller or less capitalized platforms cannot.

Natoma and the Governance Layer

The acquisition announcement that accompanied the earnings release was, in some respects, the more strategically revealing move. Snowflake signed a definitive agreement to acquire Natoma, an enterprise Model Context Protocol platform that provides governed, secure connectivity for AI agents interacting with tools, APIs, and enterprise systems.

MCP is emerging as a foundational standard for how AI agents communicate with the broader enterprise environment. As organizations move beyond isolated language model experiments toward autonomous systems that take actions, the governance layer governing those actions becomes critical infrastructure. The question of who controls access, maintains audit trails, enforces compliance, and manages the interfaces through which AI agents interact with sensitive systems is not a secondary concern; it is the central constraint determining whether enterprise AI moves from pilot to production.

Snowflake’s bet is that the platform positioned to govern both the data an agent reads and the actions it takes will occupy the most defensible position in the enterprise AI stack. CEO Sridhar Ramaswamy framed it directly: the goal is to extend the platform from a trusted foundation for enterprise data and context to become the control plane for the agentic enterprise. Cortex Code, now live across more than 7,100 accounts, and Snowflake Intelligence, whose adoption more than doubled quarter-over-quarter, are the product expressions of that ambition.

Customer Metrics and the Quality of Growth

Revenue quality matters as much as revenue level, and the customer metrics that accompanied the Q1 results support the case that Snowflake’s growth is compounding rather than broadening superficially. Net revenue retention of 126% confirms that existing customers are expanding usage. The company now counts 779 customers generating more than $1 million in trailing-twelve-month product revenue, up 29% year-over-year, with 46 crossing that threshold during the quarter alone.

Remaining performance obligations of $9.21 billion, up 38% year-over-year, provide visibility that is unusual in enterprise software and directly constrains the bear case that the current growth rate is unsustainable. More than 13,600 accounts are using Snowflake AI capabilities, with new enterprise logos including Holiday Inn Club Vacations and Houzz citing data and AI transformation as primary drivers for platform selection.

Gross margins held firm. GAAP product gross margin reached 71.0%; non-GAAP reached 75.1%. Free cash flow conversion was $232.8 million at a 16.7% margin, with adjusted free cash flow at $265.5 million and a 19.1% margin. GAAP results continued to reflect substantial stock-based compensation, producing an operating loss of $326.2 million, but for investors focused on the cash economics and operating leverage trajectory, the non-GAAP metrics are the relevant frame.

Guidance and What It Implies

Full-year fiscal 2027 product revenue guidance was raised to $5.84 billion, implying 31% growth and representing a meaningful lift from prior expectations near $5.66 billion. Non-GAAP operating margin guidance moved to 13.5% from 12.5%, and adjusted free cash flow margin is guided to 23%. Second-quarter product revenue is projected at $1.415 to $1.420 billion, implying approximately 30% growth.

Raising both the top-line and margin targets simultaneously, in the same quarter that the company announced a major acquisition and a multi-billion dollar infrastructure commitment, is a deliberate signal. Management is not funding strategic ambition at the expense of financial discipline. The revised outlook also narrows the gap between Snowflake’s growth narrative and its verifiable financial trajectory, which has been a persistent source of investor friction. For a platform that trades at a premium to the broader enterprise software sector, closing that gap is as important as any individual product announcement.

The Competitive Context

Execution risk is real. Integrating Natoma’s governance capabilities across heterogeneous enterprise environments is a complex undertaking, and the agentic AI market is developing rapidly enough that the competitive landscape will look different within twelve months. Databricks and the hyperscaler-native platforms are formidable, and enterprise spending caution has not disappeared.

What has changed is Snowflake’s strategic coherence. The company enters the second half of fiscal 2027 with a clear architectural thesis, the infrastructure commitments to support it, and financial results that suggest the thesis is finding commercial traction. For institutional investors and the senior technology leaders evaluating enterprise AI platforms, Q1 FY2027 is the quarter that made Snowflake’s argument legible. Whether that argument compounds into durable advantage will require sustained execution, but the foundation, at last, looks solid.

{kind=link}