- AI Infrastructure

- Capital Strategies

- Venture Capital

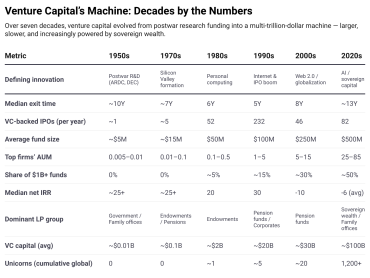

Venture Capital's Transformation:

Why VCs Are Trapped in Their Own Investments

15 minute read

As companies stay private longer and AI demands surge, venture capitalists are reimagining their entire business model—creating new ways to cash out while betting everything on one technology.

How Did We Get Here?

Venture capitalists are in a predicament. The artificial intelligence revolution requires heavy investment, so opportunities to make money have never been more abundant. But because it takes longer to exit from V.C. investments these days, cashing in on successful bets is more complicated than it has ever been.

Venture capitalists also have to live with the fact that they have underperformed the public markets recently after years of beating them. In 2022-24, the annualized return of the Cambridge Associates U.S. Venture Capital index was negative 6.4 percent, against positive 8.1 percent for the tech-heavy Nasdaq Composite. And venture capitalists’ reputation for genius has been tarnished by the disasters of V.C.-funded Theranos, FTX and WeWork.

So, venture capital is changing. It bears little resemblance to the V.C. of the 1970s and 1980s, or even to the V.C. of a decade or so ago. It has come to be dominated by a handful of giants with tens of billions of dollars in assets under management–firms that are capable of absorbing huge sums of capital from investors and deploying it at the scale required by A.I. and other sectors.

Venture capitalists are also sticking longer with their investments than they used to, partly out of choice and partly out of necessity. Companies in their portfolios that once would have sold shares in an initial public offering or been bought by another company, providing investors with a “liquidity event,” are remaining private. To satisfy the demands of investors who want money now, V.C. firms have devised clever strategies to let them cash out without an I.P.O. or a buyout.

In the process, venture capital has come to overlap with private equity. Some of the very biggest VC firms, including Andreessen Horowitz (a16z), Sequoia Capital, General Catalyst and Lightspeed, have transformed themselves into registered investment advisers, which allows them to increase their investments in private-equity-style buyouts along with crypto, debt and even publicly traded stocks. There are also big corporate venture capital operations, such as Salesforce Ventures and GV (Google Ventures).

Venture capitalists once limited themselves to nurturing young companies until they were ready to go public or be bought out. Private equity would buy mature, undervalued companies using borrowed money, manage them, and resell them for a profit. Now V.C.’s are remaining with companies longer, while private equity investors are getting in earlier. Together, blending into one another, they have lessened the need for companies to go public.

Today, startups that raise money privately have “the resources of a public company and the freedom of movement of a private company,” says Josh Lerner, a professor at Harvard Business School. As for investors, he said, “those people, for whatever reason, are wanting fewer relationships and bigger relationships.”

Some of the changes in V.C. are potentially problematic, though. Lerner says V.C.’s that get into new kinds of investing are drifting away from their expertise. And he says that while getting bigger is good for general partners, because they earn more fees, it’s not necessarily good for limited partners: “Dramatically increasing assets under management is not associated with improvement in performance. Quite the opposite.”

Where Did the Exits Go?

Issue No. 1 for venture capital funds is liquidity. “No Exit” isn’t just a play about hell by the French existentialist Jean Paul Sartre. It’s also a pretty good description of the life of venture capitalists these days. Jay Ritter of the University of Florida counted just 128 I.P.O.’s per year on average from 2020 through 2024, vs. 409 per year on average in the go-go 1990s.

“It’s hard to go public without an incredible story,” said Eric Crowley, a San Francisco-based partner in Bullhound Capital, which invests in A.I., robotics and fintech and is the investment management arm of the investment bank GP Bullhound.

In the old days, startups would get seed money, then angel investors’ money, then perhaps two or three rounds of venture capital: Series A, B and C, typically followed by an I.P.O. or a buyout. Now D, E and F rounds are common. And beyond: Anduril, a defense technology company, raised $2.5 billion in June in a Series G round that was oversubscribed.

Last year, the median age of companies that went public was 14 years, up from six years in 1980, according to Ritter’s compilation.

The drying up of the I.P.O. market doesn’t create a predicament only for venture capitalists. It’s also hard on investors in the public markets, who are locked out of big sectors of the economy that remain in private hands. The number of public companies fell to 3,804 last year from around 8,000 in 1996.

Some founders aren’t eager to go public because they dislike the strict reporting and auditing requirements imposed under the Sarbanes-Oxley Act of 2002. The JOBS Act of 2012 made their lives easier, allowing private companies with as many as 2,000 shareholders to sell shares without triggering reporting and registration requirements. The Securities and Exchange Commission is looking into letting companies report results twice instead of four times a year at the request of President Trump. But that would only slightly relieve the pressure on companies to deliver ever-improving numbers. Meanwhile, founders feel they can get all the financing they need from private sources.

Are the Workarounds Enough?

OpenAI, the creator of A.I. tools such as ChatGPT, is one example of a company that remains private even though it has enormous financing needs that once would have required raising capital on the stock market. It’s a nonprofit that owns a limited liability company that’s transitioning to a public benefit corporation. The New York Times reported in September that company documents show the company expects to lose $5 billion this year. In a staff memo in May, Sam Altman, the chief executive, said the operation “currently requires hundreds of billions of dollars and may eventually require trillions of dollars.”

Yet OpenAI has had no problem raising money from private investors, including Microsoft and various hedge funds. It has become the world’s biggest “unicorn,” valued by some estimates at half a trillion dollars, exceeding Elon Musk’s SpaceX. Unicorn is the V.C. term for a privately held startup valued at more than $1 billion, based on the notion that unicorns are extremely rare. But there were more than 1,200 unicorns worldwide as of July, according to CB Insights, an analytics firm. The new term of art is soonicorn, for companies that could become unicorns soon.

It’s nice for the unicorns that they can stay private, but what about people who don’t want to have their money tied up in them indefinitely?

Some of the people who want out are employees of the startup, who are stock-option-rich but cash-poor. Sometimes limited partners in venture capital funds, such as pension funds, foundations and endowments, need money to meet obligations to their own beneficiaries. Others might want to take cash out to invest it elsewhere–say, another company’s fundraising round. Financing for V.C.’s has dried up because limited partners who can’t extract their money from one investment can’t put money into another.

Still others who are demanding liquidity might just want to buy a nice boat, which is OK, too.

Accommodating investors’ liquidity demands has brought about one of the biggest changes in the V.C. world in recent years. Now, someone who wants out, whether a founder, an employee or a limited partner, can sell part or all of his or her position in what’s called a secondary. OpenAI, for instance, is allowing current and former employees to sell about $10.3 billion worth of their shares, CNBC reported. It said buyers would include SoftBank, Dragoneer Investment Group, Thrive Capital, MGX of Abu Dhabi and T. Rowe Price. That’s how OpenAI reached its half-trillion valuation.

Thrive Capital and other venture capital firms that have restructured as registered investment advisers have no regulatory limit on how much they can buy on the secondary market. “What used to be a backroom liquidity hack is now essential infrastructure,” Rubén Domínguez Ibar, an angel investor, wrote this year on his blog, The VC Corner.

Secondaries give sellers liquidity while giving buyers a position in a successful startup that they missed out on before, making them a win-win. “We will actively buy from insiders with permission from the company,” said Crowley, of Bullhound Capital.

Continuation funds are another solution to venture capital’s liquidity predicament. They’re another type of secondary: The fund manager or general partner spins one or more companies out of an old fund and into a new one. Often the spun-out companies are trophy properties that investors clamor for. Investors in the original fund can roll over their money into the new one or get a payout. According to the investment bank Lazard, secondary deal volume of all kinds last year was $152 billion, which was up a fifth from the previous record year of 2021.

One complication is that the general partner sets the price of the spinout as a seller, but often retains an interest in it, which creates a conflict of interest. One solution is a fairness opinion from a neutral third party.

What Happens When Everyone Bets on AI?

The most exciting thing going on in venture capital these days, the thing that’s motivating all this churn, is the boom in A.I. It was a “primordial soup” in 2024, with lots of potential but no shape, whereas in 2025 its “potential is now congealing into something real and tangible,” with its “building blocks firmly in place,” Sequoia Capital stated at the start of the year.

A.I. deals accounted for more than half of global deal value and 30 percent of completed deals through the third quarter of 2025, according to PitchBook, a data provider.

Venture capitalists are racing to lock up deals before their competitors can. The Wall Street Journal reported in August on one V.C. who met an entrepreneur at a cocktail party and was so taken with his story that he invited him to dinner that evening, followed by a party in a hotel suite. By 2 a.m., hours past the V.C.’s bedtime, he had nailed an agreement to invest $10 million in the founder’s company, “which was sealed with a handshake and pending due diligence.”

The concentration on A.I. could wallop venture capitalists if A.I. turns out to be a bubble that bursts. There’s a herd mentality on venture capital, as there is in the public markets. “Very few people invest against the grain even though they all talk about that’s what they do,” Crowley, of Bullhound Capital, said.

Even if a bust never comes, the A.I. craze is squeezing out funding for other sectors, such as consumer, education and environmental technologies. There’s a feedback loop: If the best A.I. companies are staying private longer, venture funds that want exposure to those winners must double down earlier and commit more capital. That amplifies the skew—capital isn’t just chasing A.I. generally, it’s locked up in A.I. companies for longer durations, reducing availability for other sectors.

The predecessors of today’s venture capitalists were the people who financed whaling expeditions in the mid-19th century. Americans dominated the business then, as now. Whaling “represents an important starting-point for exploring the origins of American entrepreneurship and venture financing,” Tom Nichols, a Harvard Business School professor, wrote in a case study. Today, A.I. is the white whale that V.C. is pursuing. Success is not assured.