- Digital Banking

- FinTech

- Global Banking

How Challenger Banks Are Redefining the Future of Global Finance

10 minute read

From sleek mobile platforms to borderless payments, challenger banks are reshaping the architecture of trust and power across global finance.

Bank branches, queues, and paperwork belong in another era. Neobanks have arrived, and they have rewritten the rulebook on how we access money. Today, institutions like Revolut, Nubank, and others are bypassing the constraints of legacy systems and slow-moving decision-making processes, bringing speed, simplicity, and innovation into the everyday lives of millions.

Alongside them, platforms such as Wise have fundamentally transformed cross-border transfers, reshaping expectations around cost, convenience, and transparency. Combined, their influence is redefining what it means to bank in the 21st century.

From Revolut to Nubank: Global Challengers

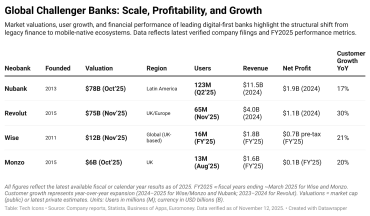

Revolut is often the headline act in this story. Founded in London in 2015, it now counts some 65 million users worldwide and generated revenues of £3.1 billion in 2024, with operating profits of £1.1 billion. Its net income stood at £790 million, a notable milestone for a digital startup. Its approach combines traditional banking services, including accounts, card payments, savings, loans, stock trading, and insurance, into a sleek mobile app that updates frequently, often on a weekly basis.

In Latin America, Nubank plays a similar role but with a distinct cultural resonance. Born in Brazil in 2013, it has grown to serve 88 million customers in Brazil alone, with an additional 6 million across Mexico and Colombia. Its pricing, transparency, and mobile-first design turned it into a digital home for millions who felt underserved by conventional banks.

On another front, Wise (formerly TransferWise) has excelled by sticking to one core mission: cross-border payments. It has turned what was once seen as a handful of charges, poor exchange rates, and long delays into something fast, affordable, and fair. Today, Wise handles almost two-thirds of its revenue through international transfers and recently reached annual processed volumes of around £145 billion. Its strategy is refreshingly focused, and in Q1 2025, it delivered pre-tax profit margins of 21 percent, well above its own targets, thanks mainly to network effects and operational efficiency.

Agility Versus Legacy

Why are these businesses so disruptive? With no branches to maintain and no outdated IT infrastructure to support, they can iterate quickly. A new feature can go live in weeks or even days. A tweak to a payment limit, a new savings goal, or an AI-powered personal finance tool can be tested, refined, and scaled with unheard-of agility.

This stands in stark contrast to the world of legacy finance. In traditional banks, changes often need to pass through multiple layers of committees, audits, and lengthy project cycles. Borrowing rates are set according to long-term planning, while process updates often weigh down innovation, and frontline agility is frequently sacrificed for governance. Neobanks, by being digital-native, sidestep much of that for the sake of speed.

“The most fundamental driver is user convenience,” Roman Eloshvili, founder of ComplyControl, an AI-driven compliance and fraud detection startup, told TECH ICONS. “Operating one of their apps today is about as easy as ordering food or calling a taxi. This simplicity of access is their biggest advantage.”

Eloshvili added that while the core products are familiar – deposits, cards, payments – the innovation lies in execution: “Neobanks have taken the previously slow and frustrating processes and made them a lot more intuitive and transparent. The real innovation of neobanks is cultural: they’ve changed what people expect from banks, and in doing so, they have irreversibly raised expectations for the entire financial industry.”

Technology not only enables rapid development, but it’s also at the core of the customer promise. Push notifications that feel conversational, instant transaction alerts, easy budgeting features, and transparent pricing all reinforce a sense of control. These are not just functional improvements but psychological ones.

Market Growth and Momentum

That narrative is backed by market growth. In 2024, the global neo- and challenger-bank sector was worth an estimated $69.6 billion, and forecasts suggest a remarkable compound annual growth rate of 26.5 percent from 2025 to 2034, with the market projected to reach $698 billion by 2034.

Of course, not all players are profitable just yet. A 2022 study estimated that there are approximately 400 neobanks worldwide, with fewer than 5 percent having achieved breakeven. Yet the most established among them – Revolut, Nubank, Monzo – are steering the ship toward sustainability. Monzo, for instance, recorded its first profitable year in 2024 with a pre-tax profit of £15.4 million and a customer base of 11 million.

Wise’s story is unique in its discipline. Since listing in 2021, its share price has risen by 36 percent, defying the typical volatility of the fintech sector. It continues to shy away from chasing the “super-app” model, instead doubling down on global payments and forging platform partnerships. Recent deals with Morgan Stanley and Standard Chartered demonstrate that banks are interested in the capabilities Wise has developed.

Marco Genaro Palma, CBDO at Swiss-based fintech company FinchTrade, told TECH ICONS, “Opening an account used to take weeks of paperwork and branch visits, while Revolut or Nubank let you do it in minutes on your phone. Going back to legacy banking feels like using a flip phone.”

The success isn’t about fancy features but about making everyday banking work the way people expect technology to work in 2025.

Palma argued that profitability separates serious players from strugglers: “Nubank and Revolut finally cracked profitability by building full financial ecosystems rather than just offering free checking accounts. The losers are still burning cash trying to grow customer numbers without clear paths to revenue. Long-term success comes from cross-selling multiple profitable products, not subsidising basic services indefinitely.”

Regulation and Reputational Hurdles

There are still critical challenges for these disruptors. Regulation is tightening, especially as incumbents lobby for stricter licensing and oversight. In the US, new rules are casting a long shadow. For UK neobanks like Revolut, Monzo, and Starling, some analysts now argue that pursuing a listing in London may be a smarter move than navigating the regulatory labyrinth of the US. Others face scrutiny around fraud protection and customer support. Revolut, for instance, has been at the centre of controversy due to complaints linked to fraud resolution – more than any major UK bank in some quarters.

“In my opinion, regulation is becoming the competitive moat that separates serious players from pretenders,” Palma said. “Getting full banking licenses requires significant capital and compliance infrastructure, which many smaller neobanks can’t afford. This actually helps established players like Revolut and Starling Bank because it raises barriers to entry while validating their business models. The regulatory scrutiny will force consolidation in the industry, leaving fewer but stronger competitors.”

Eloshvili agreed that both camps face tests ahead: “I doubt traditional banks will just outright disappear, but they will be forced to go through a transformation. We are already seeing it happen, as many banks rush to adopt AI tech and strike partnerships with fintech firms in order to boost their own capabilities. Among banks, the ones that can’t adapt will be left behind. While neobanks, as they mature, will face the same scrutiny as well-established incumbents. Those that can meet higher standards while staying flexible will be best positioned to grow.”

Resetting Expectations

Neobanks and platforms like Wise highlight how expectations have changed. Customers now expect banking to be fast, fair, transparent, and globally accessible. They expect to open an account in minutes, send money abroad at a fair rate, or apply for a loan with just a few taps on their phone.

Palma noted that the real shift is in how these players acquire and retain customers: “The innovation is in the business model and customer acquisition, not the banking products themselves. Nubank grew to a massive scale through pure word-of-mouth without spending a cent on traditional marketing. Revolut turned banking into a social platform where users can invest in crypto and trade stocks alongside basic banking.”

This is more than just competition: it is a cultural reset. These digital-first players have set new benchmarks for what banking can be. And while not every challenger will survive, those that do are likely to dictate the future of finance. Traditional institutions must innovate or risk being left behind.